In today’s lending world, credit scores often dominate loan approvals, leaving those with low scores at a disadvantage. However, new personal loan apps now assess repayment ability in a better way—considering spending behaviour, income stability, and history—making it easier for more people to get financial help.

5 Personal Loan Apps Without CIBIL Score:

Mentioned below are some of the apps which provide personal loans exclusive of your CIBIL score:

- EarlySalary

- FlexSalary

- Nira

- SmartCoin

- MoneyTap

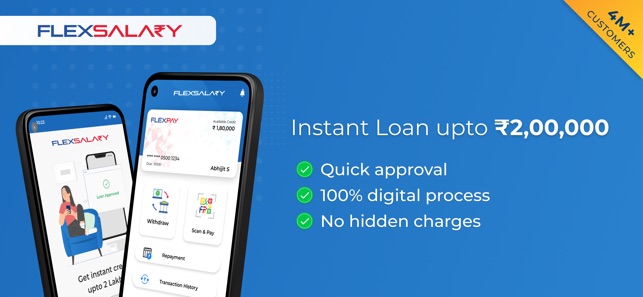

1. FlexSalary:

FlexSalary is an instant loan app specialising in the dealing of loans to consumers with a below-par CIBIL score. The disbursal of funds is seamless and instantaneous, with the whole process being completed in under 30 minutes.

This application has zero pre-payment penalty and zero charges for a bounced check. It has an interest rate ranging from 18%-54% with a tenure ranging from 10 months to 36 months (about 3 years). With an average user rating of 3.6 stars, FlexSalary, at a glance, appears to be a reliable option for personal loans, though personal discretion is always advised.

- Download Android app

- Download iOS App:

2. Nira:

Nira Finance has a wingspan of over 5000 locations and prides itself in granting loans with interest being as low as 2% and tenure ranging as long as 12 months. Like FlexSalary, it also deposits funds in less than 24 hours post-approval, thereby providing a seamless user experience. With a user rating of 4.2 stars averaged from over 292K reviews, it serves as a go-to for many loan-seekers.

- Download Android App

- Download iOS App

3. Olyv (formerly SmartCoin):

Olyv is an indigenously developed application which provides personal loans, individualized solutions to improve your credit health and pathways to boost your savings on gold stocks. With a diverse user base of over 2 crore users spread over 19000 pin codes, Olyv seems to have a favourable public verdict. Olyv also doesn’t take any collateral and has a starting interest rate of 1.5% per month. With a user rating of 4.6 stars estimated from over 317K reviews, Olyv has proven to be a reliable option for consumers.

Download Android App

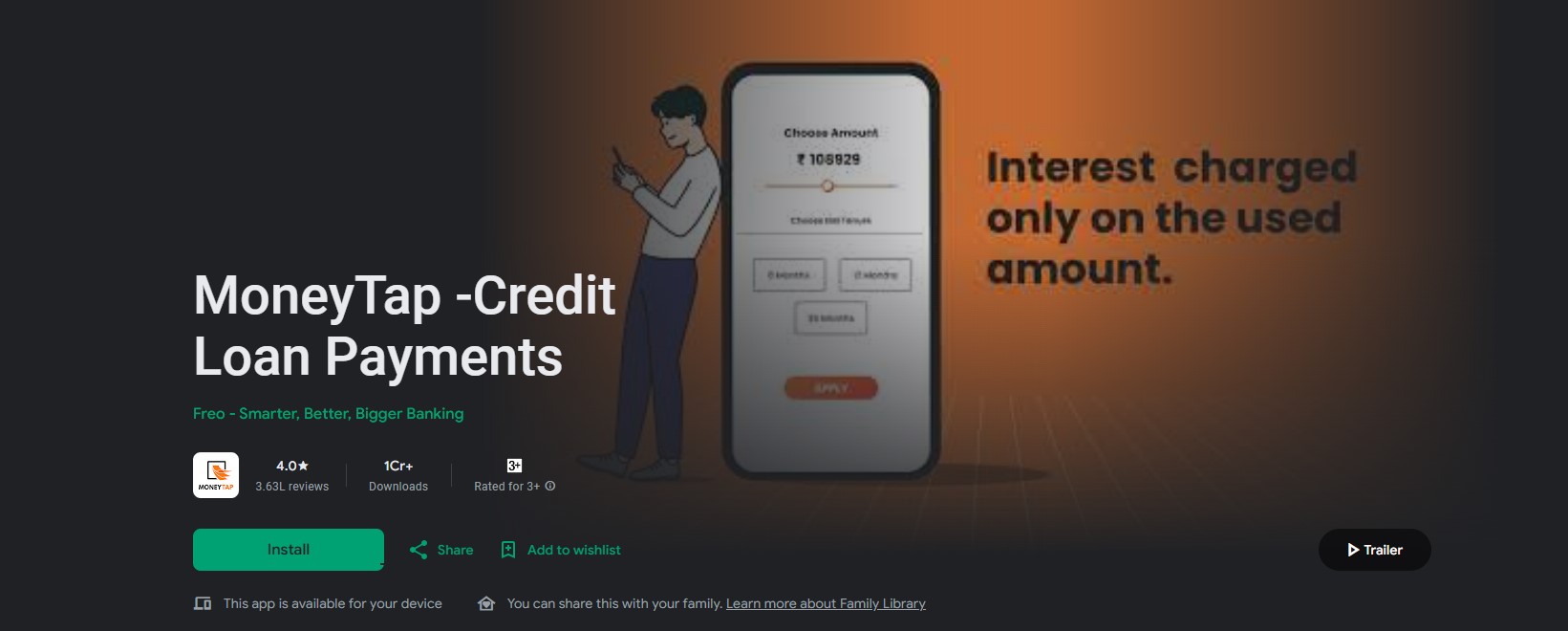

4. MoneyTap:

MoneyTap is also one of the famous apps for the personal loan. It provides a unique product line of credit, ranging from ₹35,000 to ₹5 lakhs. The key features are that it does not require any collateral for its loans, Flexible EMIs are there, does not need the CIBIL score or Credit history. MoneyTap, interest is only charged on the amount you withdraw from your credit line.

- Download Android App

- Download iOS app

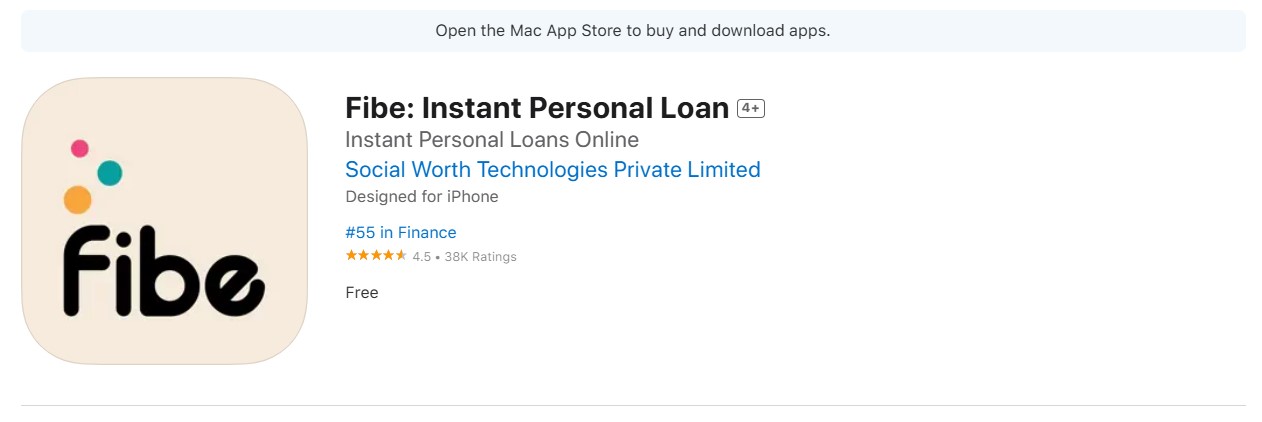

5. Fibe (EarlySalary):

Fibe (Earlysalary) is a popular digital lending platform that provides you instant loans and advances salary to the salaried person. It helps in short-term financial needs. You can get the loan from Earlysalary ranging from 8,000 to ₹5 lakhs, depending on your eligibility. Loan interest rates depend on the loan amount, tenure, and borrower profile. The starting interest rate is 18% and goes beyond that.

- Download Android app

- Download iOS App

Eligibility Criteria and Required Documents:

The eligibility criteria to apply for loans without a solid CIBIL score are rather elementary. Some of the requirements are mentioned below:

- Indian citizenship is mandatory.

- Applicant must be at least 21 years of age

- Applicants must have a stable source of income, with a minimum threshold of 15000 rupees.

- If your loan is a secured one, you must possess something which can be duly considered as collateral.

- Must have work experience of a minimum of 6 months for a salaried position and a minimum of 2 years in case of self-employment.

The list of documents required for applying for these loans is generic.

You will be required to furnish your bank statements for the last three months, proof of residence and a copy of your passport-size photograph. The requisition of any extraneous documents will be clearly mentioned on the application website.

NBFC Personal Loans for Low CIBIL Scores:

NBFC, abbreviated for Non-Banking Financial Companies, performs a more holistic evaluation of one’s repayment abilities, making it markedly different from traditional lending institutions, for whom your CIBIL score is paramount.

Companies such as Bajaj FinServ and Aditya Birla Capital can be categorised as NBFCs that provide these aforementioned loans. Though NBFCs do act as lifelines for those with near-mutilated credit scores, they do have a caveat of charging higher interest rates than traditional banks. This is due to the increased risk undertaken by these ventures by lending to those with a low CIBIL score. A summary of interest rates charged by various NBFCs is given below:

| NBFC | Interest Rate |

| Paysense | 1.4%-2.3% pm |

| KreditBee | 1.02% pm |

| Faircent | 12-28% pa |

| Incred | 16-36% pa |

| IIFL Finance | 12.75%-33.75% pa |